In 2021, diaspora Zimbabweans represented a growing share of property inquiries back home. By 2024, that figure had reached 43% of total market volume — nearly half of all buyers were sitting in the UK, Australia, the US, or South Africa, trying to buy property 5,000 miles away. This is that buyer's complete guide.

The Zimbabwe property market has a structural feature that makes it unusually legible for overseas investors: it is priced in US dollars. There is no currency conversion to navigate, no exposure to a depreciating local currency on your purchase price. A property listed at $180,000 in Avondale is $180,000 whether you are buying from Harare or Harlesden. That pricing transparency, combined with strong USD rental yields and deepening digital infrastructure for remote due diligence, has driven consistent diaspora participation to the point where offshore buyers have become the single most important demand segment in Harare's residential market.

But diaspora buyers face a specific risk profile that resident buyers do not. Distance creates information asymmetry. Urgency — the sense that you need to act quickly on a good listing before someone in Harare snaps it up — is the primary lever that fraud schemes use against offshore buyers. And the sums involved are large enough that the consequences of getting it wrong are severe. This guide is structured to close those gaps.

The Diaspora Opportunity: Why Now?

Zimbabwe's property market has converged with the diaspora investment opportunity for structural reasons that are unlikely to reverse. The Reserve Bank of Zimbabwe estimates annual remittance inflows of over $2 billion, a figure that has grown every year since 2017 and that now represents a larger share of Zimbabwe's foreign currency earnings than any single export sector. A meaningful portion of those remittances are being directed toward property acquisition.

The primary diaspora markets are, in order of inquiry volume: the United Kingdom (the largest single source), South Africa, Australia, the United States, and Canada. UK-based Zimbabweans benefit from relatively strong purchasing power parity against Zimbabwe's USD pricing — a $150,000 plot in Avondale represents approximately £120,000, accessible for buyers who have been building equity in UK property or accumulating savings over a decade-long career.

For yield-focused investors, the numbers are genuinely compelling. Rental yields in Harare's mid-range suburbs run at 7–10% in USD terms on well-managed properties. A 3-bedroom house in Mount Pleasant acquired for $180,000 and let at $1,400 per month generates a gross yield of 9.3%. Comparable-quality assets in UK commuter towns would cost three to four times more for yields of 4–5%. The combination of entry price, yield, and strong diaspora rental demand from other returnees and NGO/corporate tenants creates a compelling case.

Popular diaspora-targeted suburbs span a significant price range: Borrowdale and Borrowdale Brooke at the premium end (plots from $80,000, completed houses from $250,000), Avondale and Mount Pleasant as the mid-range sweet spot ($120,000–$220,000), and Budiriro and Kuwadzana for buyers seeking the most affordable entry points (plots from $5,000, completed properties from $40,000). The northerly suburbs dominate diaspora demand because they combine infrastructure reliability, security, and the quality of schools and shopping that returning families prioritise.

The Buying Process: Step by Step

The Zimbabwe property transaction follows a defined legal sequence. For diaspora buyers, every step in this sequence needs to be completed with additional verification layers because you cannot be physically present. Here is the process in order:

-

Set your budget and target criteria before looking at listings Establish your total budget including all acquisition costs: purchase price plus approximately 5% for conveyancing fees (3%) and stamp duty (2%), plus any renovation contingency. Define your target suburb, intended use (rental income, personal use on visits, or long-term return base), and timeline. Buyers who begin browsing without fixed parameters are most vulnerable to the urgency pressure that fraudsters apply.

-

Engage a registered Zimbabwe conveyancer before viewing any listing Your conveyancer is your most important protection. They will conduct the Deeds Registry title search, verify the seller's identity and ownership, check for encumbrances or bonds on the property, draft the sale agreement, and manage the funds transfer. Legal fees for a standard residential transaction are typically $500–$1,000 — a trivial cost relative to any property purchase. Engage them before you find a property, not after.

-

Verify your estate agent's EACZ registration All Zimbabwe estate agents are required to be registered with the Estate Agents Council of Zimbabwe (EACZ). Verify any agent's registration at eacz.org.zw before engaging. Registered agents are bound by professional standards, must maintain trust accounts for client deposits, and carry professional liability. Unregistered agents have no accountability mechanisms and cannot be pursued formally if something goes wrong.

-

Conduct an independent Deeds Registry title search Your conveyancer should run a search at the Harare Deeds Registry confirming: current registered owner, whether the title is unencumbered (no bonds, caveats, or interdicts), and whether the property description matches what you are buying. This search is public, costs a nominal fee, and takes 1–3 business days. Any seller who resists or delays this step should be treated as a red flag.

-

Arrange live video verification of the physical property Arrange a live video walk-through — not pre-recorded footage — conducted by a trusted person you arranged independently, not anyone introduced by the seller. Verify the property exists as described, is in the condition represented, and that utility bills and council rates receipts are in the seller's name. This step cannot be skipped for any diaspora purchase.

-

Execute a formal sale agreement and pay your deposit to the trust account Your conveyancer drafts the sale agreement specifying purchase price, deposit amount, due diligence period, and transfer timeline. The deposit goes to the registered estate agent's trust account — never directly to the seller, never to any individual, never via mobile money or cash. An agent who insists on any other deposit payment route is engaging in fraud.

-

Complete transfer at the Deeds Registry and pay the balance Transfer is completed by your conveyancer lodging the transfer documents at the Deeds Registry. The process typically takes 6–12 weeks from signed agreement to registered transfer. Pay the balance only after your conveyancer confirms that transfer has been registered and the title deed is in your name. Never pay the balance earlier than this confirmation, regardless of pressure from any party.

Suburb Guide for Diaspora Buyers

Borrowdale and Borrowdale Brooke represent the premium end of the market. Stand prices range from $80,000 for a 400m² plot at the periphery to $120,000+ in the established Borrowdale Brooke estate. Completed 4-bedroom houses fetch $280,000–$450,000. Rental yields are lower (5–7%) but capital appreciation has been consistent and liquidity is stronger — properties in this corridor find buyers faster when you need to exit. Preferred by diaspora buyers primarily targeting long-term capital growth and who want a premium base on return.

Avondale and Mount Pleasant are the mid-range sweet spot for most diaspora investors. Entry prices for completed 3-bedroom properties start around $130,000 and run to $220,000. Rental yields are stronger than Borrowdale — 8–10% is achievable on well-managed properties. Strong tenant demand from NGO and corporate staff, young professional families, and other returnees. The combination of yield, entry price, and suburb quality makes this the most commonly recommended first purchase for diaspora investors.

Budiriro and Kuwadzana are the affordable end, with plots from $5,000 and completed properties from $40,000. Yields are high — 10–13% is achievable — but the tenant profile is different and management intensity is greater. These suburbs suit investors seeking maximum yield who are comfortable with a more operationally demanding asset.

Using a Power of Attorney — The Right Way

Most diaspora buyers cannot travel to Zimbabwe for every stage of a property transaction. The standard mechanism for remote participation is a Power of Attorney (POA), which authorises a named individual in Zimbabwe — typically your conveyancer, a trusted family member, or a professional property representative — to execute documents and transactions on your behalf.

A POA for property transactions in Zimbabwe must be notarised: it requires formal notarisation by a notary public either in Zimbabwe or in your country of residence, followed (for POAs notarised abroad) by apostille certification under the Hague Convention. A POA that has not been properly notarised and apostilled will not be accepted by the Deeds Registry or by most conveyancing firms.

Critically, your POA should be specific rather than general. It should name the exact property, authorise the specific transactions (signing the sale agreement, paying transfer fees, accepting the title deed), and specify an expiry date. A broad general POA creates liability exposure — if the person holding the POA acts outside the specific scope you intended, your remedies are limited. Keep the POA tightly scoped.

How to Verify the Title Deed Before You Wire Anything

The most dangerous moment in any diaspora property transaction is the point of funds transfer. Fraud schemes are specifically designed to reach this moment with enough emotional investment and sunk cost that the buyer transfers funds before the verification steps are complete. The protection against this is simple: never transfer any funds until your conveyancer has provided you with a written confirmation of a clean title search result.

A clean title search result means: the registered owner is the person selling to you, the title is unencumbered, no caveats or interdicts are registered against the property, and there are no active legal proceedings involving the property. Your conveyancer should provide this in writing, citing the Deeds Registry search reference number. This is a non-negotiable precondition for any funds transfer.

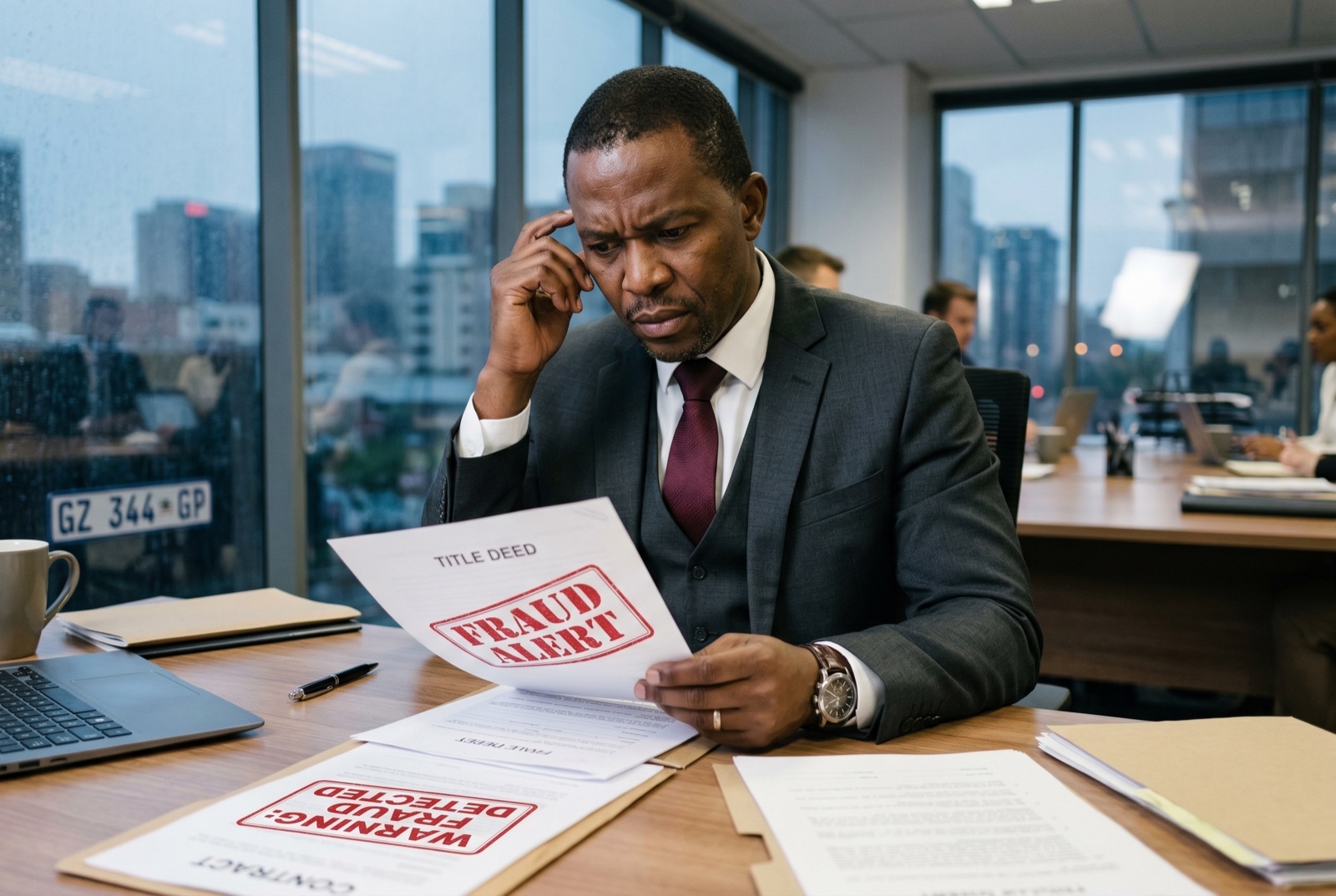

The Fraud Landscape for Diaspora Buyers

Diaspora property fraud in Zimbabwe is sophisticated and specifically tailored to the diaspora buyer's psychology. The most common schemes operate as follows:

Fake listings at below-market prices are the most common entry point. A property that would realistically sell for $180,000 in Mount Pleasant is listed on Facebook or WhatsApp at $110,000 — enough of a discount to create urgency, but not so extreme as to seem obviously fake. The listing uses real photos of an actual property (often scraped from a legitimate listing or from the owner's own social media). The first person who responds and expresses serious interest is told there are other buyers and that they need to move quickly.

Impersonation of genuine owners is the second most common scheme. The fraudster claims to own a property whose actual owner is abroad or deceased. They produce convincing-looking title deed copies (easily fabricated) and establish rapport over weeks of communication. By the time the buyer asks for a title search, the relationship feels too established to question — and the fraudster often produces a fake search result.

Developer pre-sale fraud targets buyers interested in off-plan purchases. A fraudulent developer presents plans and marketing materials for a development that either does not exist or is not progressing. Stage payments are collected until the buyer becomes suspicious — by which point the fraudster has moved on.

"Every step in this process exists because someone skipped it and paid the price. The verification process is not bureaucracy — it is the product."

Tax and Currency Considerations for Non-Residents

As a non-resident property owner in Zimbabwe, your tax obligations are real and enforced by ZIMRA (Zimbabwe Revenue Authority). The key obligations to understand before purchase are:

- Capital gains tax: 20% on the gain from residential property sales. Primary residence exemptions and inherited property carry different treatment — consult a Zimbabwe tax advisor before selling.

- Withholding tax on rental income: Rental income paid to non-residents is subject to withholding tax. Your property manager is responsible for deducting and remitting this to ZIMRA on your behalf — confirm this is happening before assuming your tax position is clean.

- Double taxation agreements: Zimbabwe has double taxation agreements with several countries including the UK, South Africa, and Australia. The specifics vary by country. A tax advisor in both jurisdictions is worthwhile for any purchase above $100,000.

- Currency repatriation: Rental income collected in Zimbabwe can be repatriated through authorised dealers. Work with your conveyancer or a Zimbabwe-licensed financial institution to establish the correct channel — informal or cash-based repatriation creates compliance risk.

Transfer costs on acquisition add approximately 5% to the purchase price: 3% conveyancing fee and 2% stamp duty. These are paid at transfer and should be factored into your total budget from the outset.

Red Flags: Walk Away If You See These

Walk away immediately if any of these apply

- Any listing priced more than 20% below comparable properties in the same suburb — this is the single most reliable indicator of a fraudulent listing

- Pressure to pay any deposit before your conveyancer has provided a written clean title search result

- Any agent who cannot produce a verifiable EACZ registration number on request

- Any seller who refuses to consent to, or delays, a Deeds Registry title search

- Any instruction to pay deposits in cash, via mobile money transfer, or directly to an individual rather than to a registered estate agent's formal trust account

- A seller who cannot produce utility bills or council rates statements in their own name for the property being sold

- Any communication that creates artificial urgency — "another buyer is viewing tomorrow," "the seller needs to travel next week," "price is being revised if not accepted today"

- A POA that has not been properly notarised and apostilled, presented as a valid authorisation to sell

The Diaspora Buyer's Verification Checklist

Before transferring any funds, confirm all of the following:

- Your conveyancer is registered with the Law Society of Zimbabwe — verify at lawsociety.org.zw

- Your estate agent is EACZ-registered — verify at eacz.org.zw

- Your conveyancer has conducted and provided a written Deeds Registry title search result confirming: registered owner identity, unencumbered title, no bonds or caveats

- You have conducted a live (not pre-recorded) video walkthrough of the property with an independent person of your choosing

- The seller has provided utility bills and council rates receipts in their own name for the property address

- Your sale agreement has been drafted by your conveyancer, reviewed by you, and signed by both parties before any deposit is paid

- The deposit instruction names the estate agent's trust account — not any individual or mobile money account

- If using a POA, it has been notarised and apostilled, is scoped to the specific transaction, and names a specific individual you trust independently of the transaction

- You have confirmed your withholding tax and capital gains tax obligations with a Zimbabwe tax advisor

- Your conveyancer has confirmed in writing that transfer is registered at the Deeds Registry before you have paid the balance

The process described in this guide adds time to a transaction — from initial interest to registered transfer typically takes 2–4 months for a well-run diaspora purchase. That timeline is not a bug; it is the fraud-prevention mechanism. Every verification step is a checkpoint that fraudsters cannot pass. Follow the process in full, without exception, on every purchase.