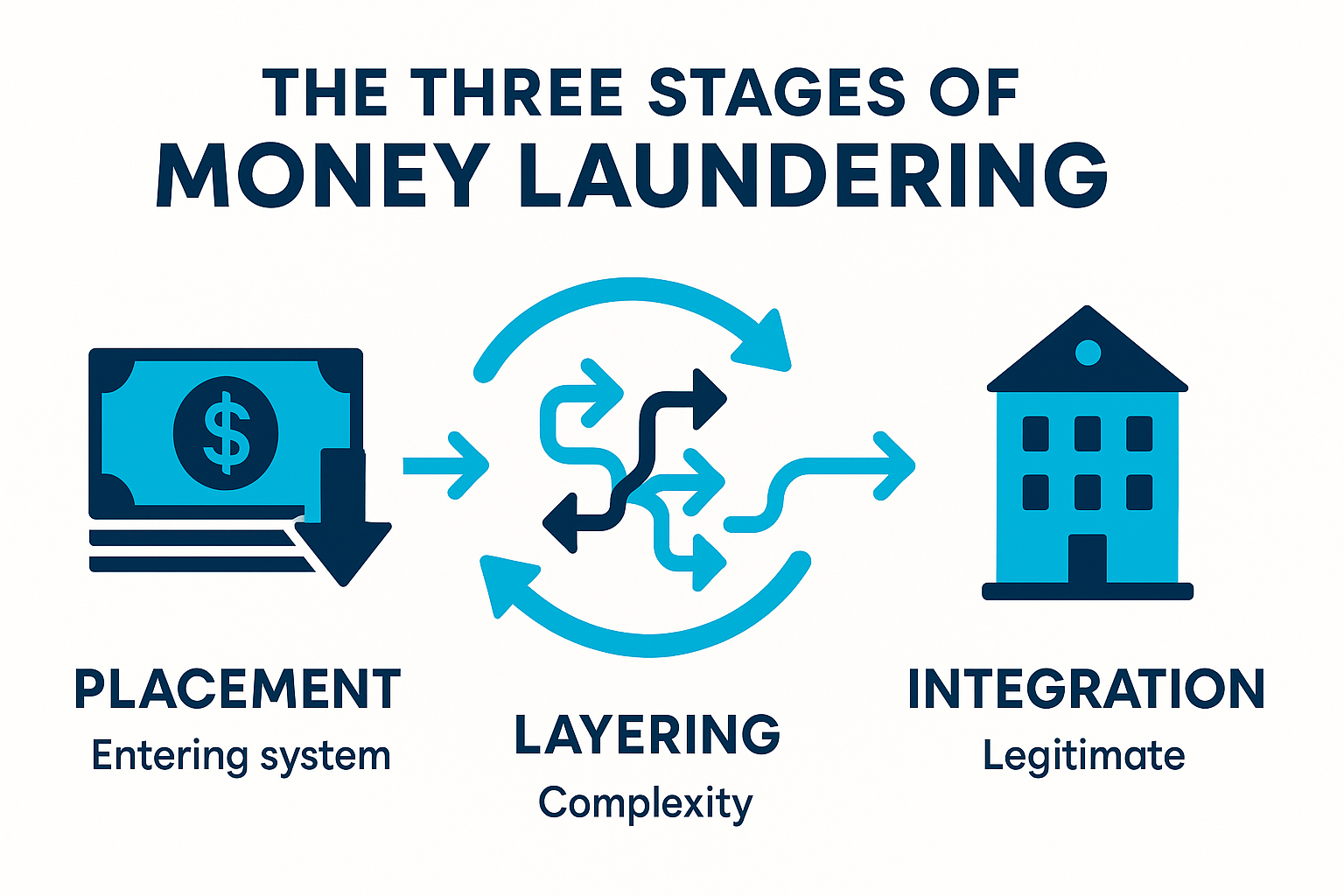

Money laundering typically follows three stages. Understanding each stage — and the methods used within them — is essential for recognising red flags in your daily work at Barclays.

Placement

Placement is the most vulnerable stage for criminals because it involves physically moving cash into the financial system, where it is most likely to be detected (Sumsub). This is the stage where front-line bank staff are most likely to encounter suspicious activity.

Smurfing (Structuring)

Breaking large sums into smaller deposits below reporting thresholds. A drug gang might recruit dozens of individuals to deposit GBP 5,000–9,000 each across multiple branches. UK Finance reports that structuring remains one of the most common typologies detected by UK banks.

Cash-Intensive Businesses

Laundering through businesses that naturally handle large cash volumes — restaurants, car washes, nail salons, convenience stores. Criminals either co-mingle illicit cash with legitimate revenue or fabricate sales entirely.

Money Mules

Individuals (often recruited via social media or dating apps) who allow their bank accounts to be used to receive and transfer illicit funds. UK Finance identified approximately 37,000 UK accounts exhibiting money mule behaviour in 2023, funnelling an estimated GBP 10 billion per year.

Young people and students are increasingly targeted for mule recruitment through social media, with promises of “easy money” for simply allowing transactions through their accounts.

Foreign Exchange

Converting currency through bureaux de change or informal value transfer systems (hawala).

Layering

Layering creates distance between the criminal funds and their source through a complex web of transactions designed to obscure the audit trail (Sumsub).

Shell Companies

Creating legal entities with no genuine business activity to move funds through seemingly legitimate corporate transactions. The UK's Companies House has been a notorious enabler, with the Economic Crime and Corporate Transparency Act 2023 introducing reforms to address this.

Multi-Jurisdiction Transfers

Moving money rapidly between bank accounts in different countries. A single sum might move through five or six jurisdictions in a matter of hours, crossing regulatory boundaries each time.

Trade-Based Money Laundering (TBML)

Over- or under-invoicing for goods and services. UK Finance highlights trade in flowers, cars, precious metals, electronics, and textiles as common TBML vehicles in the UK.

Cryptocurrency

Using mixing services or “tumblers” to obscure the blockchain trail. Criminals convert fiat to crypto, pass it through a mixing service that pools and redistributes coins, then convert back to fiat. The 2025 MLR amendments bring crypto firms into closer alignment with FSMA registration requirements.

Layered company structures — chains of companies in different jurisdictions, each owning the next — can make beneficial ownership nearly impossible to trace without international cooperation.

Integration

Integration is where laundered money re-enters the legitimate economy as apparently clean wealth. At this stage, detection is extremely difficult because the funds appear to have a legitimate source (Sumsub).

Real Estate

UK property is one of the most popular integration vehicles. An estimated GBP 10 billion is laundered through UK property annually. Criminals purchase properties with laundered funds, then sell them or collect rental income that appears legitimate.

Luxury Goods

High-value art, jewellery, vehicles, and yachts — assets that can be resold and whose provenance is difficult to trace.

Business Investments

Investing laundered funds in legitimate businesses, generating real revenue that further obscures the illicit origin.

Loan-Back Schemes

Depositing criminal funds offshore, then taking out “loans” against those deposits in the UK. The loan payments appear as legitimate debt servicing.

Case Study: The Fowler Oldfield Connection

The FCA's enforcement action against Barclays revealed a textbook layering-to-integration case. Stunt & Co, a Barclays client, received GBP 46.8 million from Fowler Oldfield — a gold dealer later convicted of money laundering. The funds moved through multiple accounts and transactions, and despite law enforcement warnings and police raids on Fowler Oldfield's premises, Barclays failed to conduct a proper review of the Stunt & Co relationship for five years.

The Fowler Oldfield case demonstrates how failures at every stage — from initial onboarding to ongoing monitoring — can allow laundered funds to pass through a major bank unchecked for years.

Match the Method to the Stage

Select a method on the left, then click the correct stage on the right. Match all 12 to unlock the next section.